Financial Leasing Companies Diverge; Asset Quality Remains Resilient Under Stress

Policy relaxation in 2007-2017 has contributed to the rapid growth of financial leasing. Large financial leases outperform small and medium-sized ones in terms of shareholder strength, asset quality and bond issuance. Large financial leases have a high concentration of assets in infrastructure industries, while non-performing assets in pro-cyclical industries (i.e. mining and manufacturing) dominate the non-performing rate of financial leases. Stress tests suggest that if China' s GDP grows by 10 % in 2021, the non-performing ratio of large financial leases will improve. Top financial leases with healthy credit profiles and overseas exposure may boost offshore issuance due to lower offshore financing costs.

Financial Lease Development Heavily Affected by Regulatory Policies

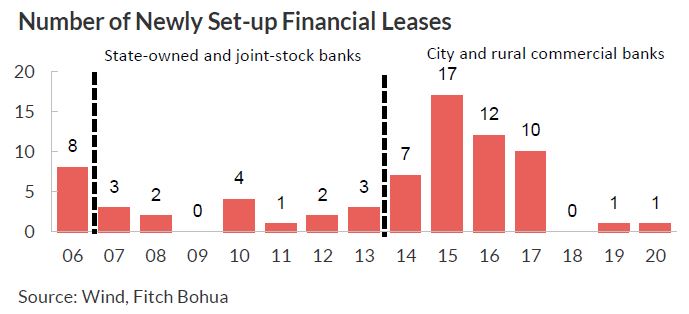

CBIRC strictly controls the number of financial leasing companies

The establishment of financial leasing companies is closely supervised by the China Banking and Insurance Regulatory Commission (CBIRC). Prior to 2007, only a small number of national or provincial government platforms were allowed to set up such entities, such as CDB Leasing, China National Foreign Trade Financial & Leasing and Hebei Financial Leasing.

The former CBRC revised the “Measures on the Administration of Financial Leasing Companies” in 2007 and 2014, respectively, allowing commercial banks to set up financial leasing companies and lowering the threshold for entry. The deregulation led to a significant increase in the number of financial leasing companies in 2007-2017.

State-owned banks and joint-stock banks established financial leasing subsidiaries in 2007-2013. From 2014 to 2017, the newly established companies were initiated mostly by urban commercial banks, rural commercial banks and industrial companies. After 2017, in the context of financial deleveraging, regulators tightened the issuance of financial leasing licenses, with only two new firms approved between 2018 and 2020. There were 71 by end-2020.

Strong shareholders enable financial leases to develop rapidly

Financial leasing companies are supervised by the former CBRC (China Banking Regulatory Commission), which requires a higher qualification of financial leasing companies’ initiators than the leasing companies administered by the Ministry of Commerce. The financial leasing industry started late, but has developed rapidly thanks to the strong financial strength of shareholders and more convenient financing channels. The proportion of their lease contract balance in the total domestic financial leasing business has increased from 12.5 % in early 2007 to 37.6 % by 2019, which is higher than that of domestic and foreign leasing companies.

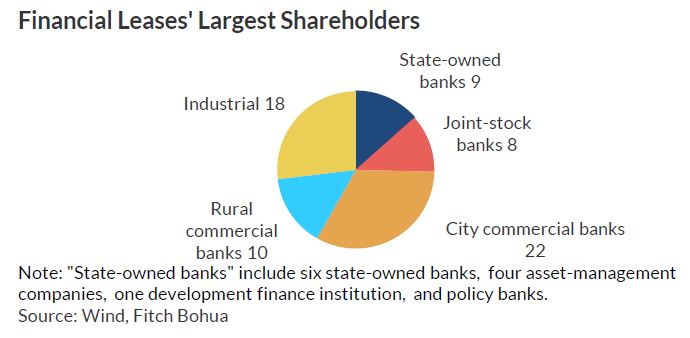

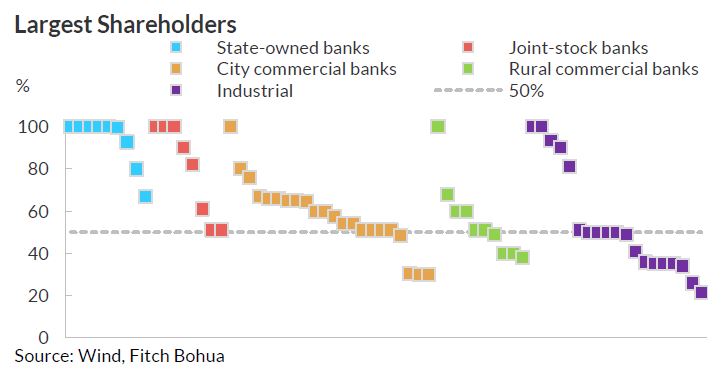

Compared with small and medium-sized financial leasing companies, the largest shareholders of large financial leasing companies are more powerful state-owned banks, asset-management companies, and joint-stock banks; they usually hold a larger stake of financial leasing subsidiaries. Under pressure, shareholders of large financial leases are more willing and able to provide liquidity and capital support.

NPAs and Financial Leasing Assets on the Rise; Non-Performing and Provision Coverage Ratios Remain Stable

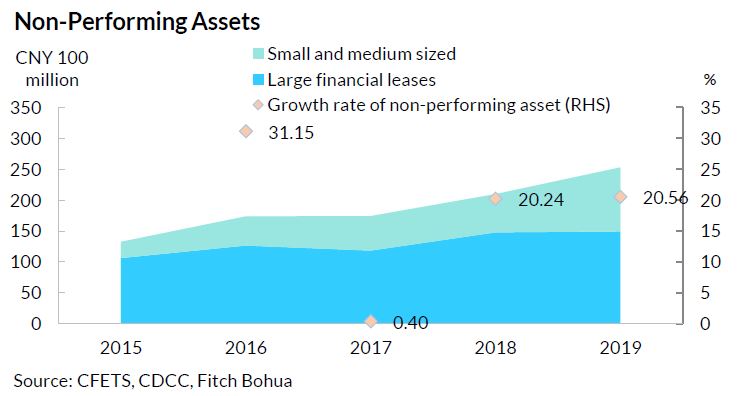

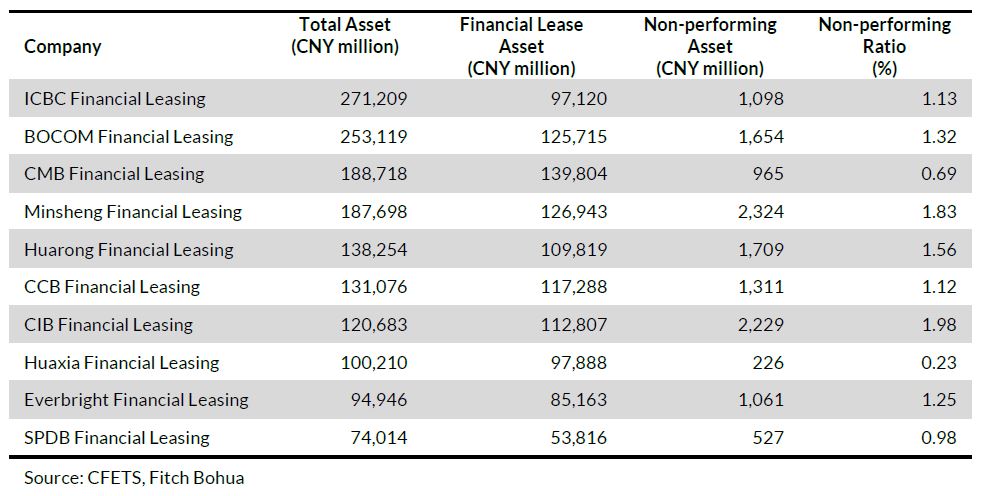

The total asset of 39 financial leasing companies that have issued debt (see Appendix I) amounted to CNY2,841.12 billion as of end-2019. We classify 10 of these firms with assets of more than CNY90 billion as large financial leasing, accounting for 61.49% of the 39 companies. They are mainly the leasing subsidiaries of state-owned banks and joint-stock banks. The other 29 financial leasing companies are classified as small and medium-sized financial leasing, mainly the leasing subsidiaries of urban and rural commercial banks.

The slow-down in global economic growth in recent years, coupled with the impact of supply-side reform policies, has exposed the long-term accumulated risks at an accelerated rate, and the scale of non-performing assets of the 39 debt-issuing financial leasing companies is on the rise. As financial leasing companies are still in a period of rapid development, the scale of financial leasing assets has also maintained a high growth.

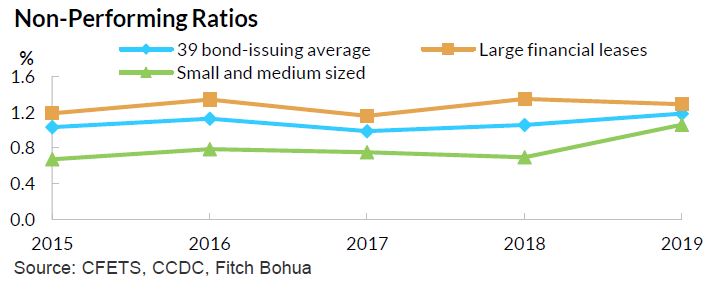

The non-performing ratio of 39 debt-issuing financial leases remained relatively stable from 2015 to 2019. The non-performing assets of 39 debt-issuing financial leases totaled CNY25.30 billion by end-2019, up 20.56% from 2018, with an average non-performing rate of 1.18%, up 0.13%. Large financial leases rely on relatively strict access standards and the risk-management system of the parent bank, coupled with their own professional expertise in specialized areas. Therefore, the growth rate of non-performing assets has been low in recent years and the non-performing rate relatively stable. The non-performing financial leasing assets of large financial leasing firms totaled CNY14.94 billion at end-2019, a small increase of 1.15% on 2018, and the non-performing rate decreased by 0.06%.

Since the revision of the "Financial Leasing Company Management Measures" in 2014, the leasing subsidiaries of city and rural commercial banks have been established one after another. With a shorter operating time, the small and medium-sized financial leases have lower non-performing assets and non-performing rates than large financial leases, which have a longer history. In recent years, the leasing business of small and medium-sized leasing companies has been accelerated and their business risks gradually exposed.

Both the non-performing assets and non-performing rate increased faster than those of large financial leases. As of end- 2019, the total non-performing asset of small and medium-sized financial leases amounted to CNY10.36 billion, up 66.70% on 2018, and the non-performing ratio increased by 0.36 percentage points to 1.06%. As the qualifications of its local Chinese customers are more fragile than for large financial leases, asset quality is likely to be hit more severely under the COVID-19 epidemic.

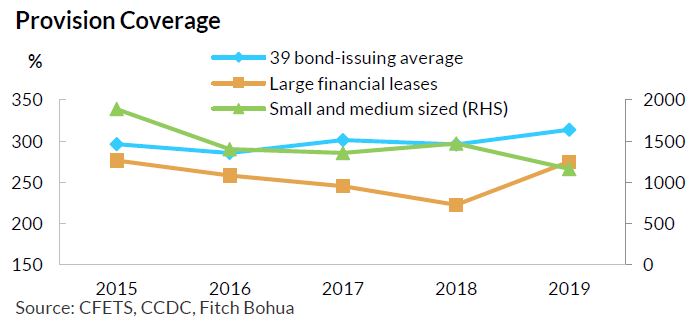

Based on the uncertainty of economic expectations, leasing companies adhere to the risk-control concept of prudent operation, and increase impairment provisions to enhance the coverage of risky assets in accordance with regulatory requirements. During 2015-2019, large financial leases made steady impairment-loss provisions and write-offs of non-performing assets. The average provision coverage ratio has remained relatively stable at 200%-300%, which is much higher than the requirements of the CBIRC, indicating a strong ability to withstand risks.

Since small and medium-sized financial leasing companies are in the start-up stage, their non-performing assets are exposed slowly. In addition, each company makes provision for impairment in accordance with the requirement of "provision/financial leasing assets" of not less than 2.5%, thus the provision coverage ratio is at a high level. Fitch Bohua expects that the provision coverage ratio of small and medium-sized financial leases will continue to show a downward trend with the development of the leasing business and continuous exposure of non-performing assets.

Asset Quality Stress Test for Large Financial Leases

High concentration in the infrastructure category of large financial leases’ leasing assets

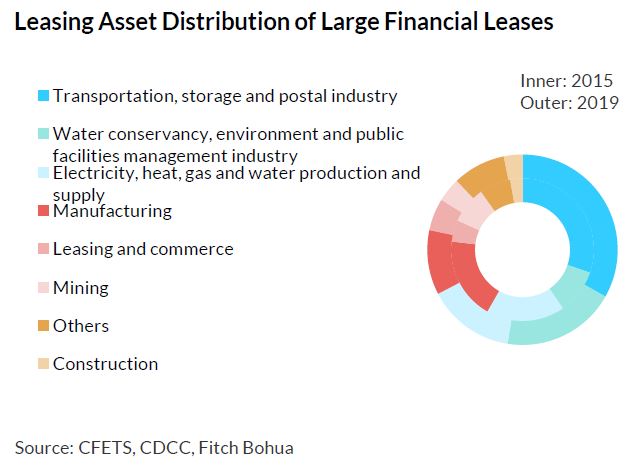

The access criteria and customer-acquisition sources of financial leasing companies are inherited from their parent banks, although the business focus of financial leases differs greatly from their parent banks. As a specialized area of the banking system, the leasing business extends the service areas of commercial banks because financial leases enjoy benefits in financing taxation and are specialized in leasing procurement, management and disposal. This specialization forms a differentiated competitiveness from the parent bank. The business fields of large financial leasing companies are mainly industries with high capital demand, such as aircraft, ships and infrastructure.

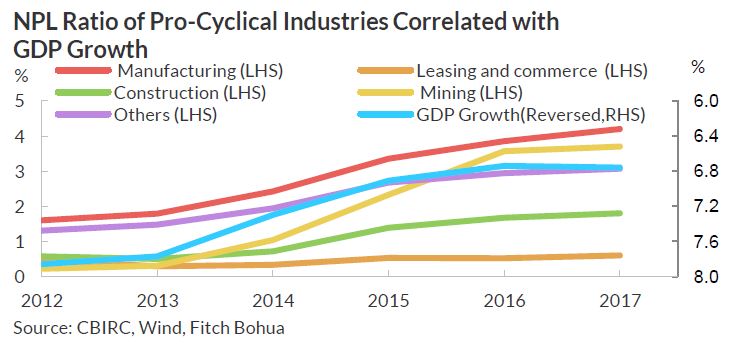

From the perspective of financial leasing asset distribution, the large financial leases’ business has remained highly concentrated in recent years. Statistics indicate that their leasing assets are predominantly in three industries: transportation, storage and postal industry (i.e. "transportation"); water conservancy, environment and public facilities management industry (i.e. "water conservancy and environment"); and electricity, heat, gas and water production and supply (i.e. "electricity and heat"). Leasing assets in the above industries accounted for 33.20%, 19.32% and 14.84%, respectively, at end-2019, much higher than that of other industries. As these industries usually play a "counter-cyclical adjustment" role in the process of economic downturn, they are less correlated with the economic cycle and therefore have more stable asset quality.

Leasing assets in the manufacturing, mining, leasing and commerce, and construction industries are significantly affected by the economic cycle, and are highly cyclical. The proportion of pro-cyclical industries’ leasing assets is significantly lower than that of transportation, water conservancy and environment, and the electric power and heat industries. The manufacturing, mining, leasing and commerce, and construction industries accounted for 10.97%, 4.10%, 5.46% and 3.15%, respectively, of leasing assets.

China's GDP growth rate was 2.3% in 2020, down 3.7 percentage points from 2019, while the credit assets of the banking sector are under pressure. The regulators have introduced timely and strong policies on deferring debt service, and increased efforts to deal with non-performing assets, with a total of CNY3.0 trillion disposed in 2020.

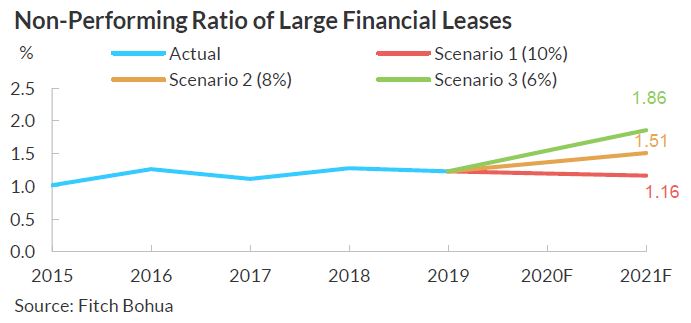

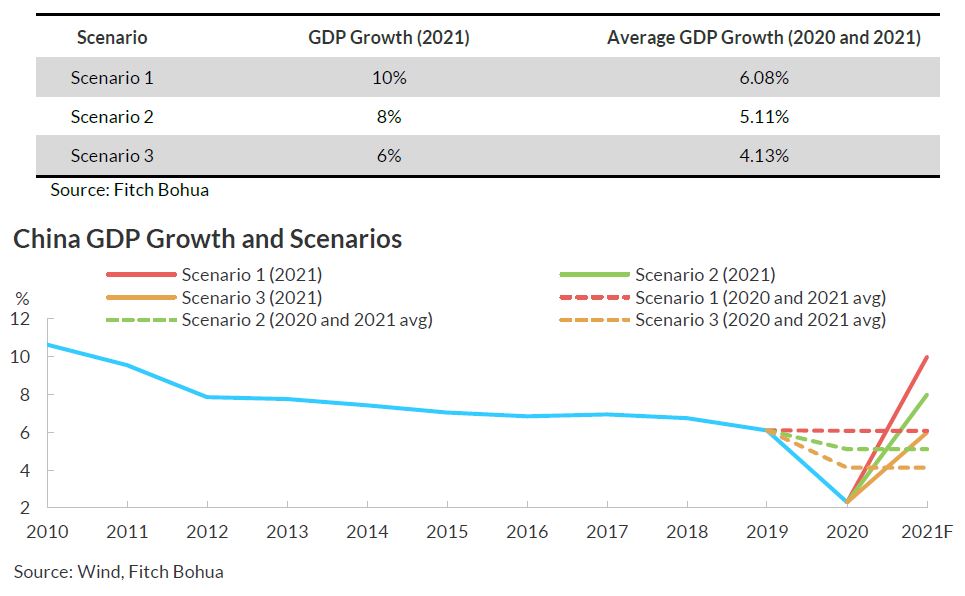

The International Monetary Fund’s (IMF) World Economic Outlook, released in January 2021, forecasts China's GDP growth to reach 8.1% in 2021. As pro-cyclical industry non-performing assets dominate the movement of financial leasing companies' non-performing rates, we conducted a stress test on the asset quality of 10 large financial leases (see Appendix II).

Pro-cyclical industry approach drives asset quality, and infrastructure assets improve the asset-quality resilience of large financial leases

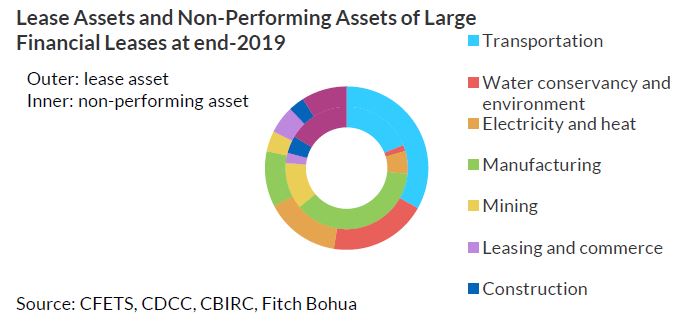

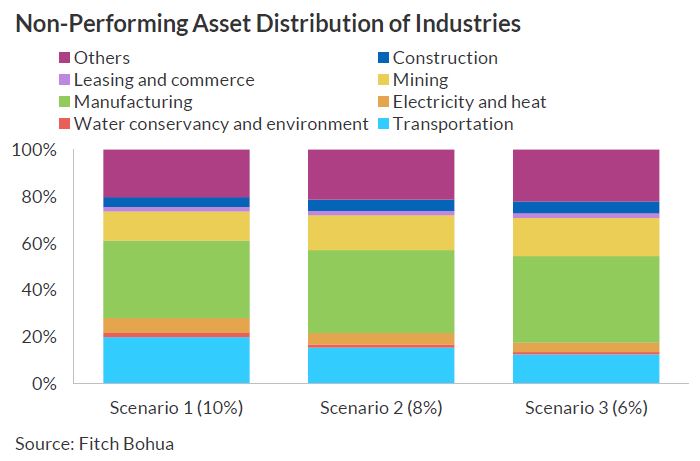

Scenario 1, China' s GDP growth rate will be 10 % in 2021 and 6.08 % on average for 2020 and 2021, which is close to the rate prior to COVID-19. Under this scenario, the economy will grow substantially in 2021 compared with 2020, and the non-performing rates in various sectors will improve. Large financial leases’ non-performing rates will fall by 0.07 percentage points, from 1.23 % at end- 2019 to 1.16 % in 2021. Manufacturing, transportation and other industries are the main sources of non-performing assets, accounting for 33.14 %, 19.96 % and 20.21 % respectively. The real-estate industry, a pro-cyclical industry, accounted for a relatively high percentage among other industries. The contributions of the water environment, leasing and commerce and construction industries to non-performing assets was low, at 1.66%, 2.02% and 4.25%, respectively.

Scenario 2 shows GDP growth of 8 % in 2021, close to the IMF' s latest forecast of 8.1 %. The average growth rate in 2020 and 2021 will be 5.11%. In this case, China' s growth rate is down 1 percentage point from 2019, continuing a slow decline. The non-performing ratio of large financial leases will rise slightly to 1.51% in 2021. The share of non-performing loans in the pro-cyclical sector, though only 32.65 % of total leasing assets, will reach 78.41 %, with mining and other sectors rising more than manufacturing and construction.

The proportion of non-performing assets in infrastructure sectors such as transportation, water conservancy, and electric power and thermal power is about 27.99%; due to the fact that infrastructure leasing assets account for 67.35 % of large financial leases, and their pro-cyclicality is weak, the asset quality of large financial leases will show stronger resistance during the economic downturn.

Scenario 3 is more cautious, with GDP growth of 6 % in 2021 and an average of 4.13 % growth in 2020 and 2012. A further slowdown in economic growth would raise the non-performing ratio of large financial leases to 1.86%. The share of non-performing assets in mining will reach 16.36%, surpassing the 12.51% of transport.

Deferment debt-service policies effectively relieved pressure on credit assets in 2020

The COVID-19 epidemic’s effect on China' s has hit credit assets in the banking sector. To cope with the shock, the central bank and other ministries and commissions jointly issued the “Notice of Temporary Delayed Repayment of Principals and Interests for SMEs” on March 1, 2020, and the “Notice on Further Implementation of Temporary Delayed Repayment of Principals and Interests for SMEs” on June 1, 2020. Banking financial institutions, including financial leasing companies, may extend the repayment period for SMEs loans due in 2020 to 31 March 2021.

According to the “China Monetary Policy Implementation Report for 2020 Q4” by the PBOC, the banking sector had extended the loan principal and interest rates by a total of CNY7.3 trillion by end-2020. The debt-deferment policies have effectively alleviated the pressure on the banking sector’s asset quality in 2020. The non-performing loan ratio of commercial banks improved slightly, from 1.86% at end-2019 to 1.84% at end-2020. Similar to the commercial banks, Fitch Bohua argues that the 2020 asset-quality metrics for financial leasing companies also benefited from deferred debt-service policies. However, the policies have not fundamentally removed the pressure on asset quality, and some of the deferred loans could still turn into non-performing assets in 2021.

A co-ordinated effort by the world's major economies to ease monetary and fiscal policy could help both the global and Chinese economies in 2021. According to stress test results, if China' s economy continues to grow rapidly in 2021, the non-performing ratio of financial leasing companies will improve and the deferred debt policy will exit smoothly. If China' s economy continues its long-term downward trend, some pressure will remain on the asset quality of financial leases. Regulatory policies may be extended if necessary to avoid a sharp rise in non-performing loans. Meanwhile, the banking sector has increased the disposal of non-performing assets in recent years through various forms such as collection, write-off and transfer, which have helped to stabilize the asset quality.

Multiple Factors Motivate Financial Leases to Seek Alternative Sources for Capital Replenishment

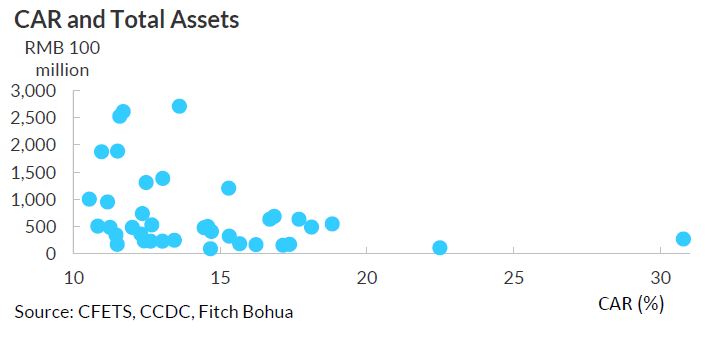

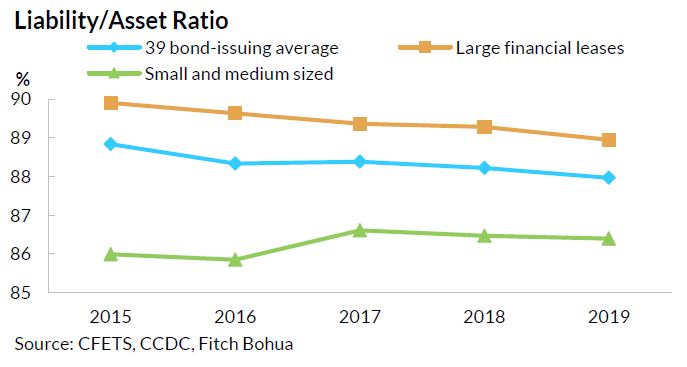

The capital consumption of financial leasing companies is related to development of the leasing business. In terms of the capital adequacy ratio (CAR) and total assets in 2019, the financial leases with higher assets generally have a lower CAR than those with lower assets. The simple average CAR of large financial leases with fast business development is 12.18 %, which is lower than that of small and medium size financial leases of 15.26 %.

As most financial leases disclose limited data, we use the assets/liability ratio to approximate their capital level. In 2015-2019, this ratio of the 39 issued financial leases declined, indicating that the overall capital level of financial leases is gradually rising. Such an increase is mainly a result of higher capital adequacy ratios of large financial leases. By contrast, with the development of the leasing business, the asset-liability ratio of small and medium-sized financial leases, with a short set-up time and abundant capital, is increasing, so the capital adequacy ratio is declining slowly.

The large financial leases’ capital levels still face pressure despite their CARs continuing to rise. On the one hand, the regulatory CAR requirements for financial leases are rising gradually, which is the main driving force behind the increase of the large financial leases CAR in recent years. In 2012, the former CBRC promulgated the Measures on the Capital Management of Commercial Banks (Trial)', which raised the CAR minimum for financial leases from 8% to 10.5%, with a transitional period of six years. On the other hand, due to the long set-up of large financial leases and the large business size, capital consumption is fast, and most are near the lower limit of CAR requirements. As a result, large financial leases continue to raise their CAR to meet rising regulatory minimums through capital growth and endogenous capital accumulation.

Financial leases with tight capital ratios had previously been able to transfer leasing assets off the balance sheet to optimize relevant ratios. However, regulators have tightened the management of off-balance-sheet assets recently, requiring such assets to be gradually returned to the balance sheet, putting pressure on financial leases’ CARs. Combined with the uncertainty brought about by the economic downturn and epidemic outbreak on asset quality and profitability, Fitch Bohua predicts that the endogenous capital sources for financial leases may be further weakened.

Financial leases will seek further capital injection from their parent banks, and bond issuance will increase. Shareholder support and the willingness of large financial leases are strong, and the financing cost is relatively low, which can help alleviate the pressure of capital replenishment. However, small and medium-sized financial leases’ have relatively weak support from shareholders, limited financing channels, and high financing costs, so they would be in a weak position to alleviate capital pressures when needed.

Bond Issuance Demand High in 2021; Offshore Issuance by Top Financial Leases May Increase

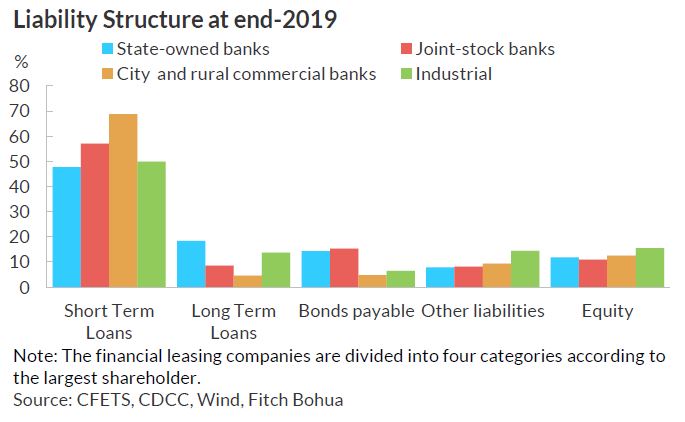

Financial leasing companies rely mainly on short-term loans from banks, but the project cycle on their asset side is generally longer, so asset-liability mismatch is common. Many firms have made an effort in recent years to reduce the mismatch by increasing the proportion of long-term borrowings and bond issuance.

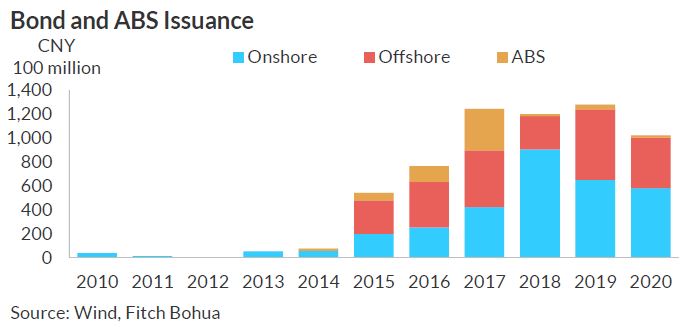

Financial leasing companies issued very few bonds prior to 2014. The “Measures on the Administration of Financial Leasing Companies”, revised in March 2014, and the “Proclamation No. 8 of the People's Bank of China and China Banking Regulatory Commission [2014]”, issued in April 2014, relaxed the criteria for financial leases to issue financial bonds in the inter-bank bond market. These policies broadened the financing channels for financial leases and ushered in a rapid increase in bond issuance. The industry raised more than CNY120 billion through bond financing between 2017 and 2019.

Fitch Bohua believes that many factors will motivate financial leases to increase bond issuance:

- The gradual relaxation of regulatory policies for financial leases to issue financial bonds and tier 2 bonds.

- Financial leases need to reduce the proportion of short-term loans and improve asset-liability mismatch.

- Monetary policy maintains a tight balance, the possibility of further easing decreases, and financing cost is difficult to reduce. Overlapping economic downturns and epidemic shocks increase uncertainty over profitability, and may weaken endogenous capital generation.

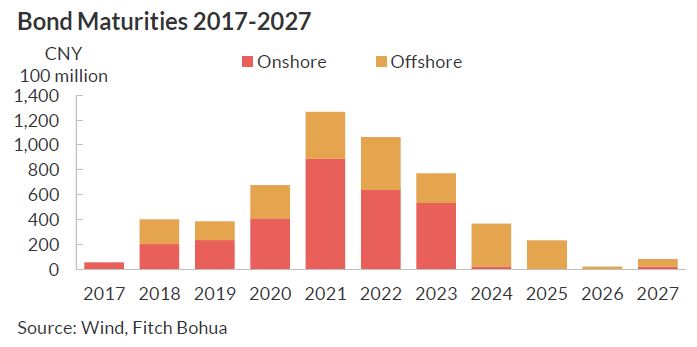

- Financial leasing companies have CNY126.7 billion of bonds maturing in 2021, twice as much as matured in 2020.

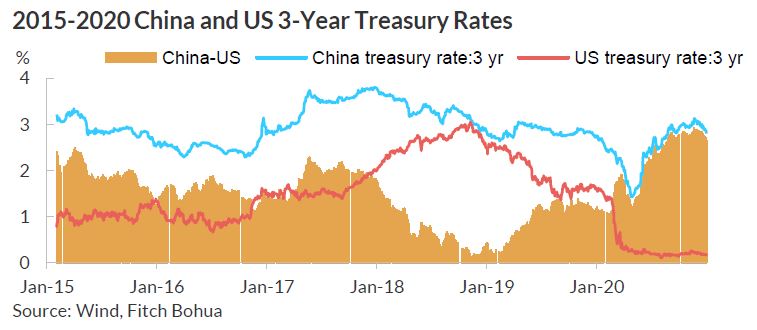

Offshore bond issuance is heavily influenced by the Sino-US interest-rate differential, and offshore borrowing costs may remain low

The ratio of offshore bonds to onshore bonds issued by financial leases is not stable. For instance, the proportion of overseas bond issuance was 52% in 2015, but only 23% in 2018. Offshore bond issuance accounted for 46% in 2019 and 41% and 2020.

Fitch Bohua believes that fluctuation in offshore bond issuance is affected mainly by the onshore and offshore financing cost difference. The difference between Chinese and US 3-year treasury yields in 2015-2017 was 172bp, meaning that the cost of overseas borrowing is significantly lower than that of domestic financing. Therefore, the proportion of offshore bond issuance by financial leasing companies is relatively high. However, the yield on US treasuries rose in 2018, and offshore financing costs rose. Thus, financial leases switched to the onshore issuance, onshore bonds accounting for 77% in that year. Offshore bond issuance has risen again since 2019 as the offshore financing cost has fallen rapidly.

Fitch Bohua expects lower offshore financing costs will attract financial leases to boost their bond offerings overseas, with the US Fed maintaining a relatively loose monetary policy and China's monetary policy likely to be tightly balanced

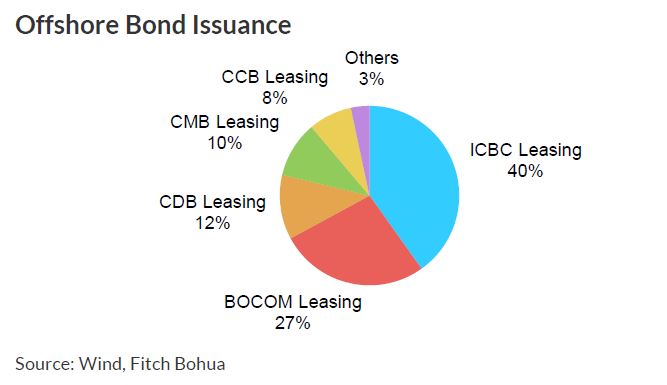

Top financial leases dominate offshore bond issuance

Statistics indicate that financial leases issued foreign bonds totalling CNY243.2 billion in 2015-2020, and issued mainly by the top financial leases. ICBC Leasing, BOCOM Leasing, CDB Leasing and CMB Leasing account for 40%, 27%, 12% and 10%, respectively. With support from strong shareholders, Fitch Bohua believes that the top financial leases enjoy a sturdy credit standing and recognition from international investors. Therefore, their offshore issuances have been generally smooth, with low financing costs. Offshore financing would also be the natural means of meeting the needs of offshore businesses since the top financial leases have more overseas business.

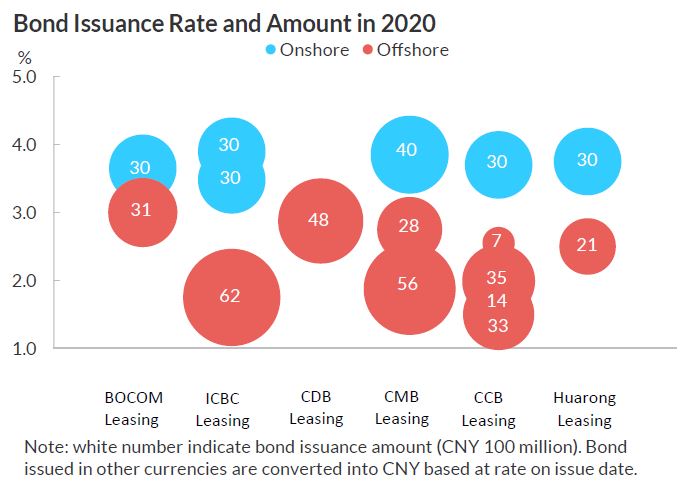

The offshore 3-year bond coupon rate was 1.50%-1.75% as issued by top financial leases in 2020, while the onshore 3-year bond coupon rate was 3.48%-3.90%. The overseas financing cost was significantly lower, which totalled CNY35.9 billion, or 1.89 times the size of the onshore bond issuance of CNY19 billion. If the US Fed maintains a loose monetary policy, the offshore financing cost should remain significantly lower than onshore, and the proportion of offshore bond issuance by the top financial leases may rise further.

Summary

The former CBRC revised the “Measures for the Administration of Financial Leasing Companies” in 2007 and 2014, respectively. The policy changes lowered the entry threshold for financial leasing companies and led to significant growth in the number, business size and bond issuance of financial leases. Large financial leasing companies have stronger shareholders, and these shareholders typically have a larger ownership. If necessary, they will be more willing and able to support the financial leases subsidiaries than small and medium-sized ones.

Statistics from 39 bond-issuing financial leases show that non-performing assets and financial lease assets are both on an upward path, and the non-performing ratio and provisioning coverage are stable. Large financial leases’ assets are highly concentrated in infrastructure sectors. The balance of finance-lease assets in transport, water and environment, and electricity and heat accounted for 33.20 %, 19.32 % and 14.84%, respectively, at end-2019, much higher than other sectors. Owing to greater macroeconomic uncertainty, changes in THE asset quality of pro-cyclical sectors (i.e. manufacturing, mining, leasing and business services, and construction) dominate the non-performing ratio of financial leases.

If China' s economy grows by 10 % in 2021, its GDP will grow by 6.08 % on average for 2020 and 2021, which is similar to the pre-epidemic level. Under these circumstances, non-performing ratios of financial leases will improve, falling by 0.07 percentage points to 1.16 % from 1.23 % at end-2019. If China's economy grows by 8% in 2021, the non-performing ratio of financial leases would rise to 1.51 %.

Regulators such as the PBOC and CBIRC have successively rolled out policies on deferred debt services, which has effectively eased the pressure on the credit assets of the banking sector, including financial leases. Fitch Bohua expects the non-performing ratio of financial leases to remain stable until the end of 2020. If the economy grows rapidly, it will help ease the pressure on asset quality, and the regulatory policies can exit smoothly. If the economic growth continues to decline, some of the deferred debt may turn gradually into non-performing assets. If this happens, financial leases will have a higher rate of non-performing assets, and the relevant policies may continue.

A combination of tighter regulation, accelerated business growth and declining endogenous profitability will encourage financial leasing companies to seek alternative ways to replenish capital. Meantime, the financial leases will have CNY126.7 billion of bonds due in 2021. Therefore, Fitch Bohua expects bond issuance from financial leases will be high. The offshore financing cost is significantly lower than that within China due to the trend of polarized monetary policies between China and US. The top financial leases, with strong credit profiles, may boost the proportion of offshore bond issuance.

Appendix 1: 39 Bond-Issuing Financial Leasing Companies

Among the financial leasing companies in China, only 39 have issued bonds. This report analyses the financial leasing companies of the following 39 bond issuers.

Appendix 2: Financial Lease Stress Test Instructions

1. Data summary of sample financial leasing companies at end-2019

2. Stress Scenario Set-up

China was the only major economy to see positive growth in 2020, with GDP rising by 2.3%, even though COVID-19 led to a sharp deceleration. The IMF, in its January 2021 World Economic Outlook, projected China’s GDP growth at 8.1% in 2021. Fitch Bohua believes that timely and strong regulatory policies effectively avoided substantial fluctuations in the asset-quality metrics of the banking sector in 2020. To avoid the uncertainty introduced by large swings in GDP growth, we combined the average growth of GDP in 2020 and 2021 in three stress-test scenarios.

The stress test is based on the correlation between GDP growth and non-performing loan ratio, including manufacturing, mining, leasing and business services, construction and others. Because the regulatory agency did not disclose the non-performing rate of financial leases, this report uses the non-performing loan ratio of commercial banks. For details of the stress test, please refer to the earlier report “COVID-19 Impact on the Asset Quality of Commercial Banks”.

Related Reports

Impact of COVID-19 on Chinese Financial Leasing Companies

Impact of COVID-19 on Automobile Leasing ABN

Impact of COVID-19 on Asset Quality of Commercial Banks

Analyst

Frank Zhang

+8610 5663 3827

frank.zhang@fitchbohua.com

Joyslin Gao

+8610 5663 3820

joyslin.gao@fitchbohua.com

Mengyuan Wang

+8610 5663 3825

mengyuan.wang@fitchbohua.com

Disclaimer

This report is based on publicly available information or research that Fitch (China) Bohua Credit Ratings Limited ("Fitch Bohua") believes reliable. However, Fitch Bohua does not represent or warrant the accuracy or completeness of such information or materials. The opinions, assessments or forecasts contained in this report reflect the judgement and views of Fitch Bohua as at the date of this report, and at different time Fitch Bohua may issue reports that contain views or forecasts that differ with those in this report.

The information, opinions, estimates or forecasts contained in this report are for information purposes only and this report does not constitute a recommendation to any person or institution to buy, hold or sell any asset; this report does not comment on the reasonableness of market prices, the suitability of any investment, loan or security (including but not limited to any accounting and/or regulatory compliance or suitability) or the tax-exempt nature or taxability of amounts relating to any investment, loan or security. This report should not be relied upon by individuals or institutions as a factor in making investment decisions. Neither Fitch Bohua nor the relevant analysts accept any liability whatsoever for any loss or damage arising from the reliance on or use of this report.

The copyright of this report is owned by Fitch Bohua. Without Fitch Bohua’s written permission, no institution or individual may reproduce, copy, publish or quote this report in whole or in part. If Fitch Bohua's permission to quote or publish this report is obtained, it must be used within the scope of permission, with attribution to "Fitch (China) Bohua Credit Ratings Limited", and this report must not be quoted, abridged or modified in any way that is contrary to its original content. Fitch Bohua reserves all its right to claim.

The terms of this disclaimer are subject to revision and final interpretation by Fitch Bohua.