Credit Analysis of Auto Finance Companies

Strategic Synergy Gradually Deepen, Weak Growth May Intensify Competition

In terms of industry, Fitch Bohua forecasts that if car sale will remain at 25.31 million in 2021-2025 as it was in 2020 auto will reach RMB2.32 trillion by 2025.

In terms of company, the asset scale and revenue of AFCs is closely correlated with brand competitiveness of the parent company. AFCs has adequate provision level and strong profitability. The asset quality of AFCs remained resilient under stress.

Auto Finance – Five-Year Forecast

China' s macroeconomic growth has slowed down in recent years. Consequently, auto sales, closely linked to household incomes, have also had a hard time. Covid-19 hit the auto market, but car sales recovered rapidly and rose modestly to 25.31 million in 2020.

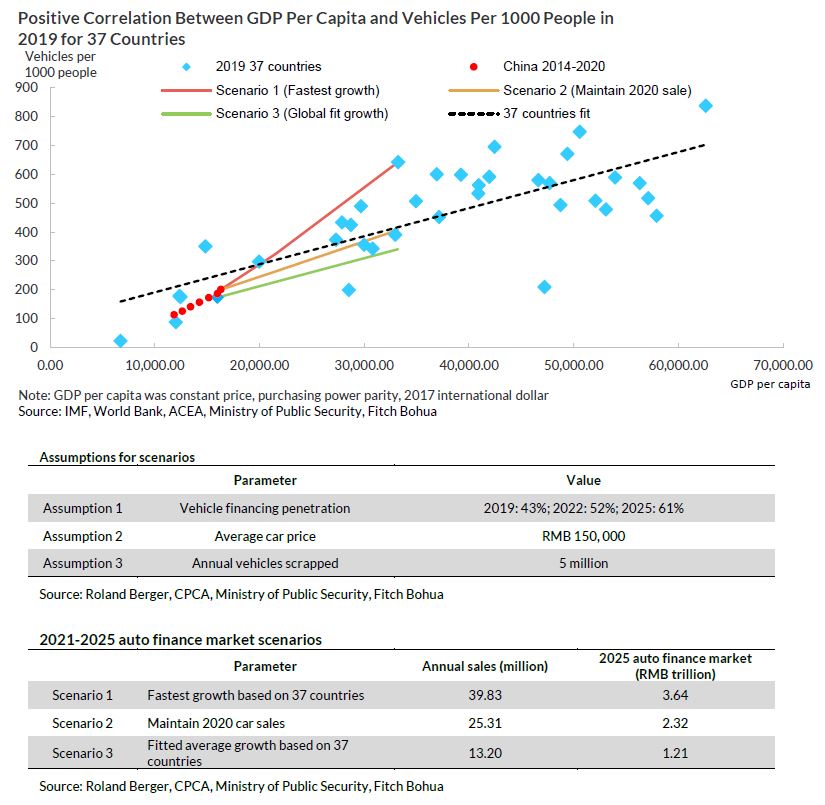

Auto sales have a direct influence on the competition and profitability of the auto-finance industry, so this report analyses the market prospects over five years, based on different sale scenarios. Fitch Bohua believes market size depends on two factors: auto sales and vehicle-financing penetration. The auto sales and auto-finance market were estimated by the correlation between GDP per capita and vehicles per 1000 people (see Appendix 1).

Scenario 1: Vehicles per thousand people grows rapidly as GDP per capita rises gradually. This scenario is the fastest rate possible based on 37 countries’ data as of end-2019. China will see average annual car sales of 39.83 million in 2021-2025, and its auto-finance market will reach RMB3.64 trillion by 2025. Such an increase in market size will definitely ease competition among auto-finance companies (AFCs) and attract more players, such as banks.

Scenario 2: Car sales will remain at 25.31 million in 2021-2025, as in 2020. In this case, the auto-finance market will reach RMB2.32 trillion by 2025. Competition among AFCs is likely to persist or even intensify.

Scenario 3: This is a slow-growth scenario, in which car sales will fall to 13.2 million per year. Correspondingly, the auto-finance market will shrink to RMB1.21 trillion up to 2025. Shrinkage will intensify competition among AFCs, and erode the earnings of AFCs and automakers. Fitch Bohua believes that China' s car sale has much room for growth, as car ownership in lower-tier cities is still at a low level. It is therefore unlikely that Scenario 3 will occur as long as the economy avoids a sharp downturn.

Joint-Stock Banks May Compete; Some Banks Cooperating with AFCs

Auto finance is a field with high entry barriers. Existing AFCs have built extensive marketing channels, professional operating experience, and close links with auto manufacturers. However, Chinese financial institutions are increasingly diversified, so AFCs may face external competition from institutions such as banks and internet platforms. Fitch Bohua believes that the outside competition comes mainly from joint-stock banks, based on the following factors:

- The auto-financing market is relatively small for large state-owned banks. For example, the market size was only 9.38% of ICBC’s total loans as of end-2019

- City and rural commercial banks are restricted to operate within specific regions, which will limit their auto-financing outreach

- Internet platforms are becoming more tightly regulated, and their ability to expand business is therefore affected.

Joint-stock banks, by comparison, with extensive retail loan experience in credit card and consumer finance, are allowed to operate without area restrictions. Meanwhile, as these banks are required to limit the proportion of real-estate loans, some may expand their auto-loan business, such as Ping An Bank and China Merchants Bank which have substantial advantages in the retail area.

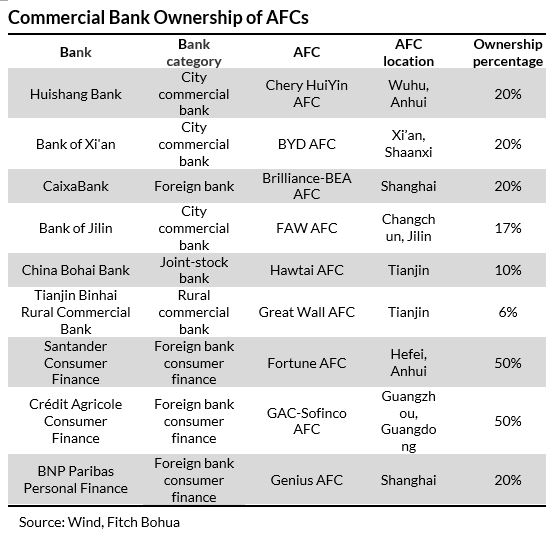

Banks could also participate indirectly in auto financing by owning part of an AFC. For instance, Huishang Bank, Bank of Xi'an and Bank of Jilin have ownership in domestic AFCs, whereas foreign banks typically take stakes of AFCs through their consumer-finance subsidiaries. This set-up ensures that an AFC could obtain financing from its bank shareholder, by sharing a small percentage of the profit with the bank.

Only a limited number of city and rural commercial banks have been able to take stakes in AFCs due to the scarcity of AFC licences and the dominance of manufacturers. Five of the banks owning AFCs are all important banks where AFCs are registered. For example, BYD Auto Finance is registered in Xi'an, where Bank of Xi’an holds 20% of its shares. FAW AFC, registered in Jilin, has invited Bank of Jilin as a shareholder, with the bank holding 17%.

The Polarization in the Industry is Prominent

Since the former CBRC issued its “Administrative Procedures for Auto Finance”, the total assets of Chinese AFCs rose from RMB10 billion to close to RMB1 trillion. According to the China Banking Association, the total asset of Chinese AFCs reached to RMB906.37 billion by end-2019.

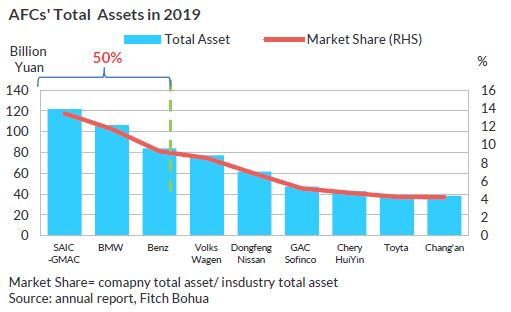

In terms of size distribution, the intensifying concentration in the automobile industry resulted in differentiation of the AFCs. The total assets of the top AFCs such as SAIC-GMAC, BMW exceeded RMB100 billion. The proportion of total assets of the top-five AFCs was 50%. The polarization in the industry will continue, considering the top AFCs own ‘first-mover advantage’, high business maturity and strong shareholder support.

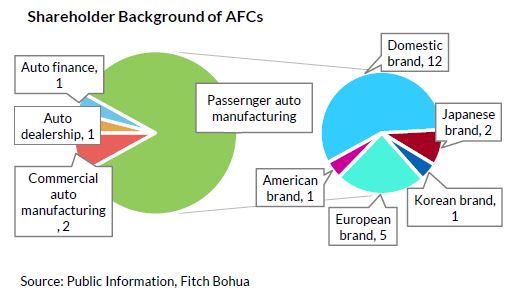

AFCs, as a form of non-bank financial institutions offering financial service to automobile buyers and dealers, have strong industrial characteristics. The number of registered AFCs in China reached to 25 by end-2019. The shareholders are from auto manufacturing, dealership and financing. Those shareholders from passenger auto manufacturing dominated, at 21.

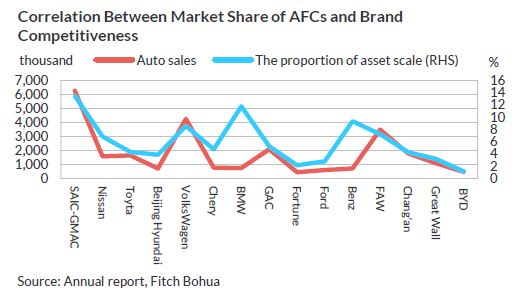

The main responsibility of AFCs is to provide credit and finance service to the parent company brands, which means that the business of AFCs is largely affected by brand sales. According to annual reports of AFCs in 2019, the proportion of total assets has a strong correlation with the sales volume of the parent companies.

Provision Level Adequate, Overdue Loan Rate Improving

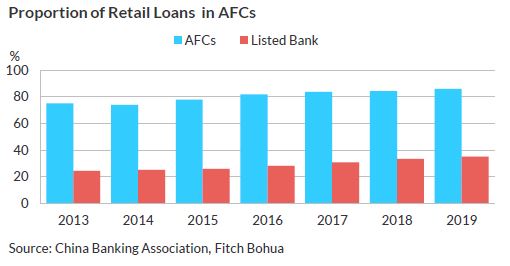

As opposed to corporate loans which are predominant in commercial banks, retail loans are a major force in the development of AFCs, thanks to the huge amount of auto-retail customers from parent companies. The proportion of auto credit scale has continued to increase since 2013. The retail loan balance of AFCs reached RMB71.94 billion by end-2019, accounting for 86.3% of total loans while the average proportion of retail loans of the listed banks was only 35.13%.

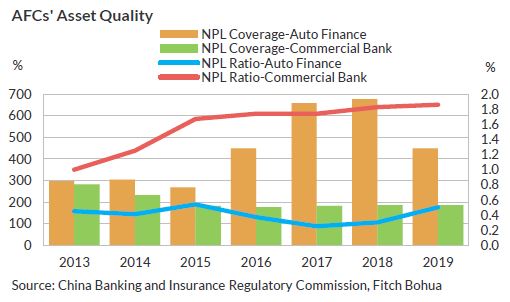

Retail loans are characterised by being widely dispersed, and AFCs always use cars as collateral. Auto-loan risk is relatively low, according to the non-performing loan (NPL) ratio of all industries in 2017, published by the former CBRC. The asset quality of auto loans is inferior only to housing mortgage loans. The fact that auto loans dominate in AFCs results in high asset quality. The NPL ratio has been maintained at less than 1% in recent years – the auto-finance industry’s NPL ratio was 0.5% in 2019, lower than that of commercial banks at 1.86%. At the same time, AFCs are also prudent in the provision. NPL coverage decreased from 677.5% in 2018 to 448.6% in 2019 despite the macroeconomic downturn. Yet , the provision level of auto finance was still adequate compared with that of commercial banks (186.1%) during the same period.

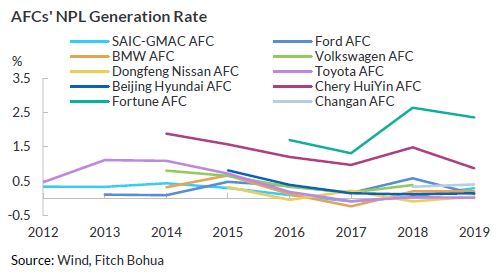

In terms of the NPL generation rate of AFCs, the rates of domestic brands are higher than those of foreign brands. In 2019, the average NPL generation rate of both Chery AFC and Fortune AFC exceeded 1% while that of foreign brands was maintained below 0.3%. The divergence of asset quality of AFCs is clear.

The business operations of auto enterprises were affected considerably by Covid-19 in 2020. On the other hand, the halted production resulting from Covid-19 also reduced the willingness and ability of consumers. According to the data in 2Q20, the negative impact of Covid-19 on auto industry also transmitted to the auto-finance industry. Fitch Bohua’s interbank auto ABS index showed that the M2 overdue rate increased to 0.3% in 2Q20, 200% higher than at end-2019. Asset performance improved with the acceleration of the Chinese economic recovery in 2H20. The M2 overdue rate fell to 0.09% by end-2020, which was flat compared with end-2019.

Asset Quality Remains Resilient under Stress

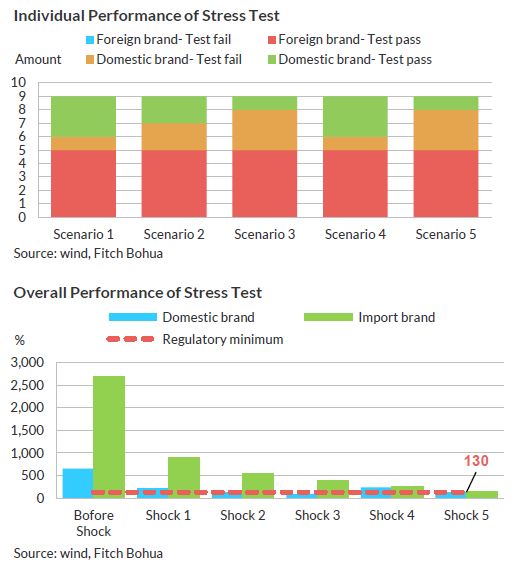

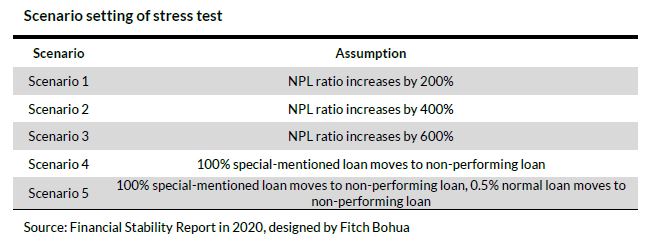

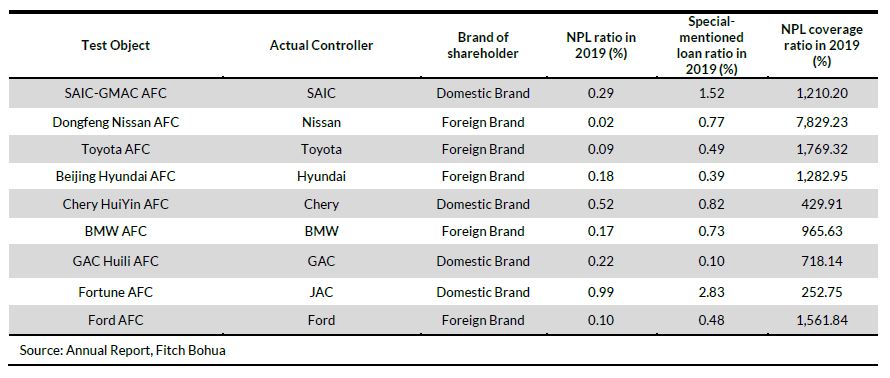

In order to research the ability of Chinese AFCs to resist risk under extreme scenarios. Fitch Bohua designed a stress test for AFCs, referring to the Chinese Financial Stability Report issued by People’s Bank of China (PBOC) in 2020. The test sample includes nine AFCs (the asset scale of nine AFCs accounted for 55% of the total in 2019). The sample is divided into domestic and foreign brands, and the test is to evaluate the NPL coverage ratio under five stress scenarios. If the NPL coverage ratio of test objective is higher than supervision standards (130%), the test will be considered as passed (see Appendix II).

In terms of overall performance, the average NPL coverage ratio of domestic and foreign brands reached 652.8% and 2,681.8%, respectively, by end-2019. The NPL coverage ratio of AFCs performed well under stress, thanks to adequate provision levels. Under all testing scenarios, the NPL coverage ratio of both domestic and foreign brands fulfilled supervision standards (130%). As for individual performance, foreign brands performed better under stress. All foreign brand samples passed the test, versus only one domestic brand.

In total, the provision level of all tested samples was adequate, but the performance between domestic and foreign brands diverged under stress.

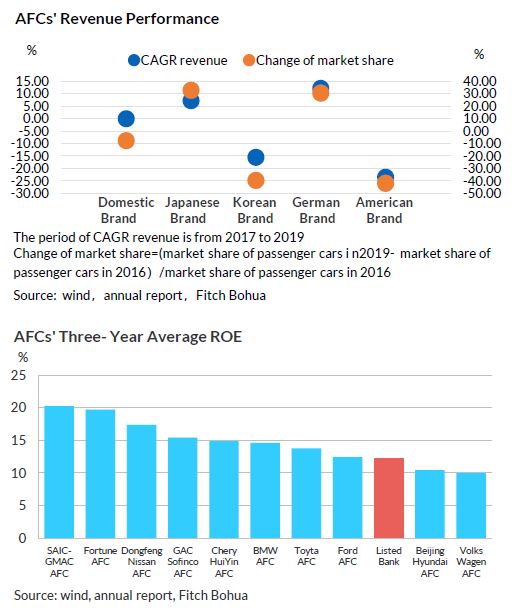

Revenue Largely Affected by Change of Brand Market Share

Auto brands have a large impact on the business of AFCs. In order to research the financial performance of AFCs, Fitch Bohua selected 10 AFCs and divided them into five categories (see Appendix III).

The total revenue of sample enterprises is closely correlated with their auto parent companies. The revenue of AFCs with related brands performed well in recent years, benefitting from a rising market share of German and Japanese brands whose three-year compound growth rate rose to 12.3% and 14.0%, respectively. In comparison, the revenue growth of AFCs with Korean and American brands was relatively weak, with the three-year compound growth rate of Korean brands at only -9.11%.

We expected that AFCs with Japanese brands would increase more than other brands, considering that the sales volume of Japanese brands performed well in the passenger auto market in 2020. Looking forward to 2021, the differentiation of brand image and consumer preference will result in divergence within the auto industry, as mentioned in the auto industry outlook. Fitch Bohua believes that the divergence of auto industry may also transmit to the auto-finance industry.

As for profitability, the operating revenue of AFCs is from interest income. AFCs have strong bargaining power with auto loans. High bargaining power and low impairment costs propel the strong profitability of AFCs. The average ROE of AFCs was higher than that of listed banks from 2017 to 2019. The ROE of SAIC-GMAC AFC even exceeded 20%.

Parent Injects Capital Continuously

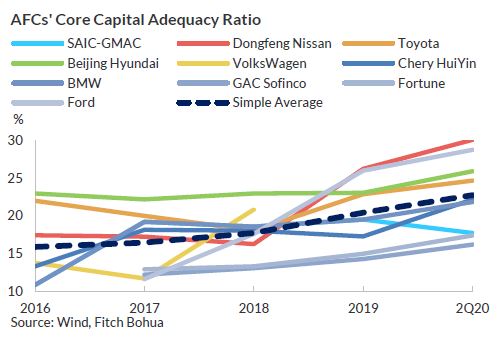

Expected loss for AFCs is offset by reserves, and unexpected loss is often offset by capital. Consequently, the risk-bearing capacity of a company is determined by the level of reserves and capital. According to “Administrative Procedures for Auto Finance” issued by former CBRC in 2008, the capital adequacy level of AFCs should be no less than 8% while the core capital adequacy level should be no less than 4%.

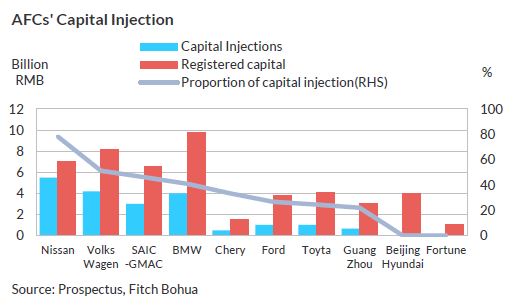

The capital level of 10 sample companies has increased continuously in recent years thanks to several capital injections from shareholders. The average core capital adequacy ratio of sample companies reached 22.7% By the end of 2Q20, which is much higher than the regulatory baseline. The capital level of most sample companies has kept rising even after the Covid-19 shock . Among them, t Japanese and Korean brands are generally higher than the average. The core capital adequacy and capital adequacy level of Nissan reached 30.0% and 31.2%, respectively. In comparison, domestic brands were relatively low. The CBIRC introduced related documents in 2020 to encourage AFCs to issue secondary capital bonds in order to strengthen capital.

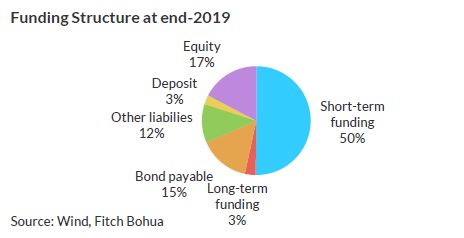

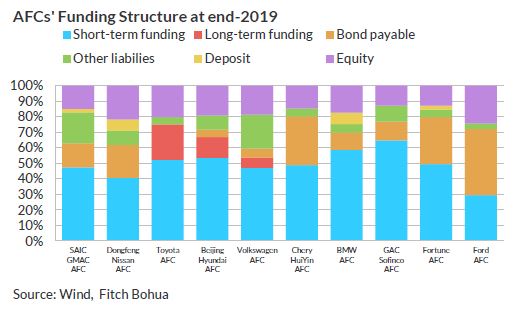

Reliance on Short-Term Financing; Funding Structure to be Optimized

Statistics indicate that short-term financing accounted for 50.2 % of the total funding for 10 sample AFCs. AFCs may face short-term debt-servicing pressure due to their high reliance on short-term loans and borrowings from banks and other financial institutions. To relieve this pressure, there are two measures that AFCs could take. One step would be to ensure adequate bank credit lines. A second would be to optimize the financing structure by increasing the ratios of long-term borrowing and bonds payable, which would strengthen the resilience of debt-servicing capabilities and improve the financial position. Bonds payables and long-term borrowings were 15.1% and 3.1%, respectively, of total funding at end-2019.

Although AFCs generally rely on short-term funding, debt structures are not identical for all AFCs. Short-term borrowings account for only 29.5% of Ford AFC's financing structure, which is significantly lower than the industry average. Meanwhile, bonds payable and stockholders' equity combined account for 66.9% of total funding, making its debt structure more resilient.

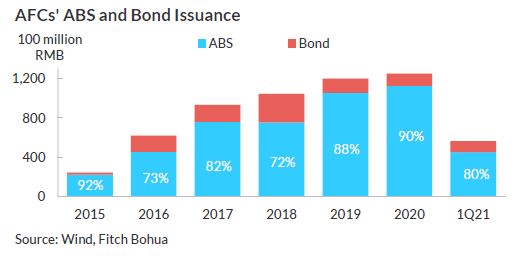

ABS and financial bonds, as long-term liabilities, help to improve the asset-liability maturity mismatch of AFCs. ABS issuance was RMB112.4 billion in 2020, accounting for 90% of total debt issuance. ABS is therefore a more utilised instrument by AFCs than bond issuance (with issuance of only RMB12.5 billion in 2020). ABS issuance grew rapidly from 2015 to 2020, with an average annual compound growth rate of 38.1%. Boosting bond issuance may further optimize AFCs’ funding structure, given that ABS has reached a large scale.

AFCs Play a Strategic Role in the Group Company

The share proportion of auto enterprises in 25 registered AFCs reached 85% by end-2019. Auto finance, as an important phase in the auto industry chain, can directly stimulate brand sales of the group company and also promote growth of auto consumption. Auto finance in China has played an important part in sector development.

From the perspective of asset size, the proportion of auto-finance business of a domestic brand in the group company exceeded to 14%. The asset proportion of Fortune AFC even reached 45% in 2018.

From the perspective of sales volume, the Chinese auto consumption market has become an important source of revenue for global auto enterprises. Other than Hyundai, the sales volume proportion of most foreign auto brand shareholders in China exceeded 10% and has displayed a rising trend. We believe that the growth in brand sales will improve the asset size of the auto-finance business of foreign brands in China, and then in turn raise the willingness of the group company to support.

From the perspective of capital injections, the shareholders of top AFCs including Nissan, Volkswagen, SAIC-GMAC and BMW have a relatively strong willingness to support. The proportion of capital injections of such companies in the last three years has got up to 40%. The capital injection proportion of Nissan even reached 78.3%. Continuous capital injections are not only out of a need for scale expansion but also out of strong confidence in the development potential of the auto-finance market.

Fitch Bohua believes that the developing maturity of the Chinese auto-finance market will mean that the strategic synergies of an AFC with its parent company will become increasingly prominent. At the same time, the Matthew Effect on asset scale of AFCs will also diverge the support willingness of shareholders to some extent.

Appendix:

I. Auto Finance Market Forecast Assumptions and Scenarios

Statistics indicate that GDP per capita and vehicle per thousand people exhibit a strong positive correlation in 37 countries. Accordingly, this report sets out three scenarios and estimates for China’s auto-finance market by 2025, based on International Monetary Fund (IMF) forecasts of per capita GDP and population. In addition, the China vehicle financing penetration rate increases gradually from 43 % in 2019 to 61 % by 2025, according to Roland Berger’s 2020 China Auto Finance Report.

II. Stress Test Description

i. In the scenarios of the stress test, if the initial NPL ratio is A%, the B% ‘special-mentioned’ loan moves to NPL and the NPL ratio increases by N%, so the new NPL ratio will equal (A+B+N) %.

ii. The test is designed by Fitch Bohua referring to the current situation of AFCs and the Financial Stability Report of 2020. All the test results are based on the macroeconomic data and annual reports of AFCs in 2019, and are irrelevant to the stress test in Fitch Bohua’s rating criteria of non-bank financial institutions.

iii. Since the auto-finance industry is easily affected by auto-industry prosperity and macroeconomic cyclical fluctuations, and with the very high loan concentration of AFCs, Fitch Bohua assumes that the deterioration in asset quality of AFCs will be more serious in extreme conditions than that of commercial banks.

Stress Test List

Related Research

Impact of COVID-19 on Auto Finance Companies and Auto Loan

Interbank Auto ABS index in 4Q20

Fitch Bohua Industry Outlook: Auto Production

Analyst

Norman Sheng

+8610 5663 3826

norman.sheng@fitchbohua.com

Joyslin Gao

+ 8610 5663 3820

joyslin.gao@fitchbohua.com

Frank Zhang

+8610 5663 3827

frank.zhang@fitchbohua.com

Disclaimer

This report is based on publicly available information or research that Fitch (China) Bohua Credit Ratings Limited ("Fitch Bohua") believes reliable. However, Fitch Bohua does not represent or warrant the accuracy or completeness of such information or materials. The opinions, assessments or forecasts contained in this report reflect the judgement and views of Fitch Bohua as at the date of this report, and at different time Fitch Bohua may issue reports that contain views or forecasts that differ with those in this report.

The information, opinions, estimates or forecasts contained in this report are for information purposes only and this report does not constitute a recommendation to any person or institution to buy, hold or sell any asset; this report does not comment on the reasonableness of market prices, the suitability of any investment, loan or security (including but not limited to any accounting and/or regulatory compliance or suitability) or the tax-exempt nature or taxability of amounts relating to any investment, loan or security. This report should not be relied upon by individuals or institutions as a factor in making investment decisions. Neither Fitch Bohua nor the relevant analysts accept any liability whatsoever for any loss or damage arising from the reliance on or use of this report.

The copyright of this report is owned by Fitch Bohua. Without Fitch Bohua’s written permission, no institution or individual may reproduce, copy, publish or quote this report in whole or in part. If Fitch Bohua's permission to quote or publish this report is obtained, it must be used within the scope of permission, with attribution to "Fitch (China) Bohua Credit Ratings Limited", and this report must not be quoted, abridged or modified in any way that is contrary to its original content. Fitch Bohua reserves all its right to claim.

The terms of this disclaimer are subject to revision and final interpretation by Fitch Bohua.