China Financial Institutions Monitor – 1Q21

Moving Out of COVID-19

- China was the only major economy in 2020 to achieve positive GDP growth, and is likely to experience high economic growth in 2021

- The deferred debt-servicing policy will expire at the end of March, but a negative impact on commercial banks’ asset quality is likely to be minimal

- CBIRC has lowered the requirements for bulk transfer of non-performing assets; disposal of non-performing assets by commercial banks is likely to accelerate

- The insurance industry has maintained an adequate solvency margin ratio for a long time, and the launch of the Phase II Project of China Risk Oriented Solvency System is likely to bring positive results for the industry

- ESG is increasingly valued in China, and ‘green finance’ is of rising importance

China’s Economy Beats Expectations in January-February, Signalling a Positive Outlook for 2021

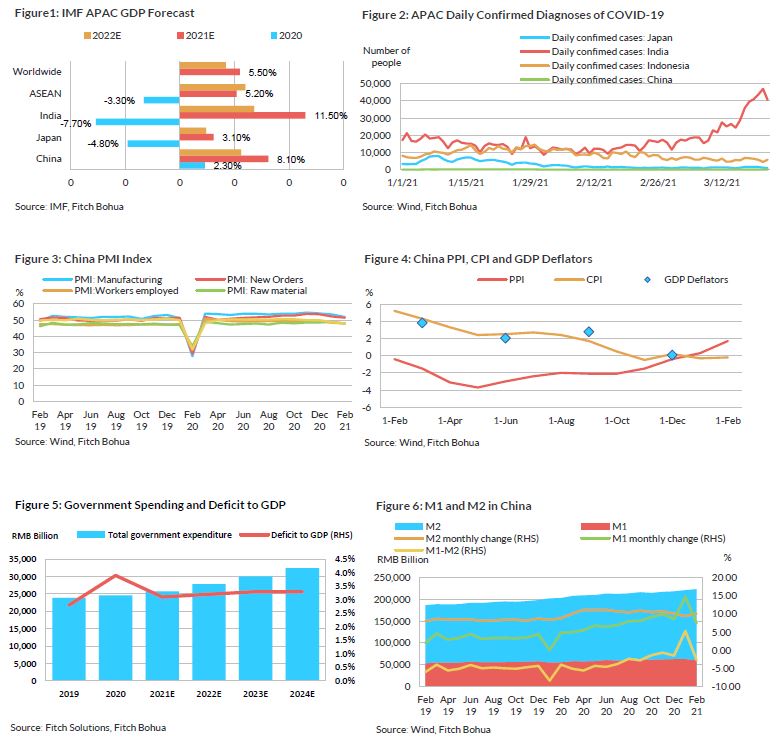

The Asia-Pacific (APAC) region as a whole experienced economic contraction as a result of Covid-19 In 2020. Major economies such as Japan, India and the ASEAN-5 1 countries experiencing significant economic recession with GDP growth of -4.8%, -7.7% and -3.3% 2.

China was the only major global economy to achieve positive economic growth, thanks to its relatively stringent Covid-19 control measures and an effective economic stimulus plan. GDP growth was 2.3%, with total GDP exceeding CNY100 trillion.

The number of new infections per day has peaked in most countries in the Asia-Pacific region except India, and is in a decline, based on the latest Covid-19 infection data. Economic growth in APAC emerging markets is likely to be more optimistic in 2021 with the rollout of Covid-19 vaccines.

The latest IMF forecasts point to 3.1%, 5.2%, 11.5% and 8.1% for Japan, ASEAN, India and China, respectively. China is forecast to grow by 10.59% of GDP over the two-year period of 2020-2021, well ahead of India (2.91%) and other APAC economies.

China's PMI Index in expansionary range for the 12th consecutive month, PPI-CPI on a diverging trend

The PMI Index in February 2021 was above that of the same period in 2016, 2018 and 2019, and was in an expansionary range. Meanwhile, China's CPI fell, thanks to a year-on-year decline of 14.9% in pork prices.

The PPI has been on an upward trend for nine consecutive months by end-February 2021, the. The index fluctuations have mainly been affected by the recent sharp rise in crude oil prices. Commodity prices such as non-ferrous metals have also risen by different degrees as domestic demand grows.

Fitch Bohua believes that CPI and PPI are displaying a diverging trend, illustrating a certain imbalance in economic recovery: food and services prices are stable, but prices for manufacturing goods still fluctuate. As domestic demands continue to expand, the overall price level for 2021 will return to a healthy and reasonable range with minimal risk of massive inflation.

China’s import and export trade performance was strong in January-February, with the "export substitution" effect remaining a strong supporting factor

Both import and export values exceeded market expectations significantly. Fitch Bohua believes developed economies are likely to see a large recovery in manufacturing activities, hence weakening China's import dependence. The "export substitution" effect is likely to diminish over in 2021, while new orders and demand will also come in and continue to support China’s export trade performance as developed economies resume commercial activities. On the import side, the value of imports is likely to grow for some time to come as domestic production capacity remains strong and commodity prices move higher, but regional and international relations may bring some uncertainties.

Highlights of Key Events and Policies

China sets GDP growth target for 2021 at 6% or above

The 2021 Government Work Report sets the GDP growth target for 2021 at 6% and above. According to the latest forecast by Fitch Ratings, China's GDP growth rate for 2021 will be approximately 8.4%. Fitch Bohua believes the 6% growth target takes into account the risk of a potential resurgence of Covid-19 and reflects the government's intention to promote structural transformation in the economy, and achieve objectives such as supporting employment and stabilising consumer prices.

The recovery of the Chinese economy in 2021 will be supported by a number of favourable factors. First, the steady rollout of Covid-19 vaccines and the successful measures that brought the epidemic under control in China create favourable conditions for businesses to resume commercial activities. In addition, the government's continued efforts to stimulate domestic demand and reduce financing costs for SMEs, as well as the lower GDP base in 2020, also create a positive starting point for an economic rebound.

Fitch Bohua believes the improvement in economic fundamentals will drive the overall financial market towards an upward cycle: as businesses resumed commercial activities, demand for credit continued to grow, pushing the debt-to-GDP ratio in January-February to a level exceeding expectation.

Debt rose moderately in February. Monetary policy is moving toward a "tighter balance", while remaining flexible and targeted

The Chinese Central Bank (PBOC) had not injected liquidity into the market for three consecutive weeks as of 24 March 2021, and its overall open market operations appeared prudent. The M2 growth rate returned to above 10% after recording 9.4% in January.

Fitch Bohua expects that PBOC’s open market operations using instruments such as the medium-term lending facility (MLF) in mid-February has dismissed market concerns about short-term illiquidity. Judging from the movements of market interest rates, it is unlikely that the PBOC will raise interest rates in the short term: the 7-day reverse repo rate and the 1-year MLF have remained unchanged for 11 consecutive months.

In order to mitigate the impact caused by Covid-19, the Chinese government adopted a relatively accommodative monetary policy in 2020. The policy had a positive impact in effectively mitigating the impact of the pandemic on the economy, while it also caused a significant rise in debt.

Money supply will be tightened to some extent compared with 2020 as the government increasingly emphasises a targeted and neutral monetary policy. Fitch Bohua expects a move towards a tighter balance throughout 2021, but for liquidity in the short run not to be significant reduced.

Government deficit to be reduced to 3.2% in 2021; fiscal policy to emphasise sound economic development and policy sustainability; government spending to favour technology and media industries

In terms of fiscal policy, the government's deficit rate for 2021 is aimed at around 3.2%, down from the 2020 target of 3.6%. Fitch Bohua expects that the main objectives of fiscal policy in 2021 are to maintain the necessary spending level while withdrawing gradually from some of the short-term Covid-19 supportive measures implemented in 2020. A key theme in the 2021 fiscal policy is to return to the pre-Covid long-term policy objectives, which include improving people's livelihood and promoting structural transformation of the economy to be focused more on technology and media.

According to Fitch Solutions’ forecasts, annual fiscal spending will continue to grow, with higher spending on long-term policy objectives. However, government revenues will also improve with the steady recovery of the Chinese economy, and therefore the government fiscal deficit rate is likely to remain roughly within the 3.1%-3.3% range in the longer term.

Banks maintain a tightened lending policy to real estate

Some Chinese cities have continued a tightened lending policy to real-estate companies in 1Q21. As stated in the 2021 Government Work Report, the main objectives of such measures are to ensure house-price affordability to the public, reduce speculation in the housing market, and stabilise prices.

In light of these measures, Fitch Bohua expects the banking sector's lending to real estate will continue its previous tightening trend in 2021. PBOC and the China Banking and Insurance Regulatory Commission (CBIRC) had previously jointly issued the “Notice on the Establishment of the centralised Management System for Real Estate Loans for Banks” ("Centralised Real Estate Loan Management System" hereinafter), which specifies the upper limits of loans which can be granted to real-estate companies and home mortgages for various banks. The Centralised Real Estate Loan Management System has come into effect in 2021, significantly limiting the flow of credit into the real-estate sector.

Some real-estate companies which had expanded excessively and with high leverage have been highly exposed to liquidity risks since 2020. The implementation of the Centralised Real Estate Loan Management System will further reduce the growth of real-estate loans in the banking sector, producing a positive impact on the ‘real economy’ finance costs and benefiting the long-term development of the banking sector.

The deferred debt-service policy is likely to have a minimal impact on commercial banks and non-bank financial institutions’ asset quality

According to data published by CBIRC, the banking sector had granted emergency loans of CNY24.27 billion to small, medium and micro enterprises (MSMEs) and foreign trade enterprises as of December 2020, and the amount of loans applied for deferred repayment was CNY6.6 trillion, accounting for 4.5% of the total loans granted by the banking sector.

The non-performing loan (NPL) ratio of commercial banks was 1.84%. Based on this figure, Fitch Bohua expects that some of the deferred repayment loans will turn into NPLs; and if banks continue with the current write-off policy, this will lead to a 10bp-69bp increase in the NPL ratio, giving banks a negative impact on asset quality. (See: Banking Industry Asset Quality Analysis and Outlook: Delayed Exposure of Non-Performing Loans to Small and Micro Enterprises, Asset Quality of Municipal and Rural Commercial Banks May Come Under Pressure (银行业资产质量分析与展望:小微企业不良贷款延缓暴露,城商行及农商行资产质量或承压))

The overall provisioning coverage ratio of commercial banks was 184.5%, which was generally adequate and able to withstand shocks from asset¬ quality deterioration.

Fitch Bohua believes that the original regulatory requirement to reduce the provisioning coverage ratio for small and medium-sized banks has effectively eased the pressure on increasing provisions for bad loans for small and medium-sized banks, though it has not fundamentally eliminated the risks of asset-quality deterioration of these banks. The banking industry has generally already made adequate provisions for deferred repayment loans, and the related losses have been reflected in their financial statements. Therefore, It is likely that the end of the deferred debt-service policy will not have a further strong impact on the profitability and asset quality of the banking industry.

On 24 March 2021, the Chinese State Council decided to extend the deferred debt service policy to the end of 2021, with companies and banks negotiating case-by-case to decide on the extension period. Fitch Bohua believes that the extension of the debt-service policy will delay the credit risk exposure of some MSME loans. The flexibility of allowing independent negotiation between companies and banks on repayment can effectively spread the credit risk exposure over a reasonable timeframe, thereby helping commercial banks to better manage risks while alleviating the repayment pressure on MSMEs.

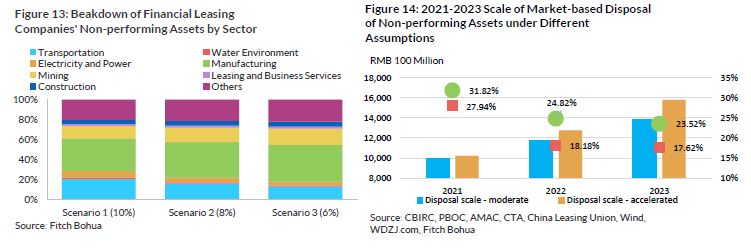

As for non-bank financial institutions, the deferred debt-service policy has eased the pressure of asset-quality deterioration in pro-cyclical industries assets such as manufacturing, mining, leasing and business services. The asset quality of large financial leasing companies is likely to remain resilient. As the monetary policies of China and the US show a divergent trend, the cost of overseas financing is significantly lower than that of the domestic route, and some of the leading financial leasing companies may leverage their good credit standing and increase the scale of overseas bond issuance. (See: Increased Differentiation among Financial Leasing Companies, Asset Quality Remains Resilient under Stress Scenario(金融租赁公司分化明显,压力情景下资产质量保持韧性))

CBIRC has lowered the requirements for bulk transfer of non-performing assets; disposal of non-performing assets in 2021 is expected to reach a record high

In January 2021, the CBIRC issued the “Notice on the Commence of Pilot Programme for Non-Performing Loans Disposal” (《关于开展不良贷款转让试点工作的通知》), which formally launched the pilot programme for bulk transfer of corporate and personal NPLs within a single account. The pilot programme allows bulk transfer for assets including personal consumer loans, credit card overdrafts and personal business loans that were included in the non-performing category. Under previous regulations, personal non-performing loans were not allowed to be transferred in bulk, and NPLs to corporates had to be bundled together with more than three accounts before they could be transferred in bulk packages. The pilot programme not only broadened the range of non-performing asset transfers, but also relaxed the threshold amount for bulk transfers of non-performing assets.

At present, banks have relatively limited means to dispose of personal non-performing assets, and rely mainly on debt collection, write-offs, debt restructuring, transfers and asset securitisation. There is a pilot programme that permits personal non-performing loan asset securitisation, although the amount of assets disposed in this way is still relatively low. Currently, bank credit, trust assets and receivables from non-bank financial institutions are still the main sources of non-performing assets in China, accounting for over 80% of the total.

With China's economy undergoing a structural transformation and still in the process of recovering from the impact of Covid-19 epidemic, the scale of supply of non-performing assets (including non-performing bank loans and accounts receivable of corporates) has shown rapid growth. It is likely that the source of non-performing assets will diversify gradually in the future, as the capital market has seen an increasing amount of bond defaults. In the next three years, non-performing asset disposal is likely to reach a peak, with average growth of more than 20%. (See: Local AMC credit watch: deep ploughing the local market, regional differentiation is obvious, the future of non-performing assets market disposal ratio will increase (地方AMC信用观察:深耕本地市场,区域分化明显,未来不良资产市场化处置占比将提升))

In addition, 2021 is the last year of the transition period of the "Guidance on Regulating the Asset Management Business of Financial Institutions" (《关于规范金融机构资产管理业务的指导意见》; "New Regulation on Asset Management" hereinafter). The new rules stipulate that the off-balance sheet non-standardised non-performing assets can not be transferred into new asset-management products, and can only be dealt with by including into banks’ balance sheets or disposal in the market. Fitch Bohua expects that the end of the transition period of the “New Regulation on Asset Management” will create pressure for the disposal of non-performing assets, and there will be large-scale off-balance sheet non-performing asset disposals in the second half of 2021. Fitch Bohua believes the relaxing of regulations of non-performing assets bulk transfer will help accelerate the disposal of banks' non-performing assets and bring benefits and stability not only to individual banks but the entire financial system.

The non-performing corporate and personal loans being bulk transferred reached CNY657 million by 1 March. Fitch Bohua expects the market will see more bulk transfers of personal non-performing loans from the second quarter 2021.

The insurance industry has maintained an adequate solvency margin ratio, and the launch of the Phase II Project of China Risk Oriented Solvency System will bring a positive impact

The solvency margin of China's life insurance industry has been on a downward trend since 2018, but the decline has been minimal; the overall claims paying ability for the sector remains strong. Covid-19 brought particular downward pressure on the solvency margin ratio of China's life insurance industry, but the figure rebounded in 4Q20 and the comprehensive solvency margin ratio was maintained above 235%, highlighting the industry’s sufficient capital buffers and strong risk resilience (See: Fitch Bohua's Industry Outlook 2021: Life Insurance (惠誉博华2021年行业展望:人身险))

For property insurance companies in China, the solvency margin ratios of most small and medium-sized property insurance companies were at a high level, according to their quarterly solvency reports, due mainly to their slow business development (especially non-vehicle insurance, which tends to consume large capital). By contrast, the solvency margin ratios of large insurance companies tend to be lower than those of their SME counterparts, as large insurance companies have more established business, which consume more of their capital. In this case, large insurance companies in China generally have a greater need for bond issuance. Most debt-issuing insurance companies have annual premium income of over CNY10 billion, except for Beibu Gulf Insurance and Yingda Taihe Property Insurance.

For small property insurance companies experiencing high business growth and with a need to improve solvency, it is actually difficult to refinance through bond issuance, as some may not meet the regulatory requirements or the interest rate may not look favourable. Most active bond issuers from the insurance industry tend to be industry leaders with high profitability and proven debt-service capability; these companies usually have higher debt, while other insurance companies maintain low leverage. (See: Fitch Bohua's Industry Outlook 2021: Property Insurance (惠誉博华2021年行业展望:财产险))

Digital currency pilot programme accelerates, as government experiments with technology under different application scenarios

On 14 August 2020, the Chinese government issued the "Plan for Deepening the Pilot Programme for the Innovative Development of Trade in Services" (《全面深化服务贸易创新发展试点总体方案》), proposing to carry out a digital RMB pilot project in Beijing, Tianjin and Hebei, the Yangtze River Delta Region, the Guangdong-Hong Kong-Macao Greater Bay Area, and some of the central and western regions. The pilot project has been accelerated since the beginning of 2021:

- Beijing: 50,000 digital currency red packets were distributed for testing, with a total of CNY10 million

- Suzhou: The "Digital RMB - Suzhou New Year Festival Jingdong Special Session" campaign was launched on 5 February, with CNY30 million worth of digital currency red packets distributed locally

- Shenzhen: The Shenzhen Local Financial Supervision Bureau issued several measures to support the financial development in Luohu District as well as distributing digital currency coupons for gold jewellery purchases.

- SWIFT, together with several Chinese payment clearing agencies, established the Financial Gateway Information Service Company in Beijing on 16 January. The main business of the company will include information systems integration, data processing, consultancy in technology, and data processing

The local governments of Beijing, Shanghai and Guangdong have included the digital RMB pilot project in their government report for 2021 and in the outline of their 14th Five-Year Plan. Recent news shows the scope of digital RMB testing is expanding. It is likely that digital RMB’s application scenarios will be gradually enriched during the 14th Five-Year Plan period.

Fitch Bohua believes that currently digital RMB is still in its infancy; the pilot project mainly tests its function as a payment tool, and the scale of the testing is relatively small. However, it is likely after the completion of the current pilot project that the digital currency might be applied into other areas for further testing.

ESG is increasingly valued in China, and ‘green finance’ is rising in importance

In recent years, ESG(Environment, Social and Governance)has become increasingly valued in China. ESG encourages companies to take responsibility in issues related to environmental, social and corporate governance, thereby promoting long-term sustainable development. In August 2016, the Chinese government issued the "Guidance on Building a Green Financial System" (《关于构建绿色金融体系的指导意见》), which requires all listed companies to make mandatory disclosure of environmental information by 2020. Fitch Bohua expects that ESG information disclosure requirements will continue to expand in the coming years, and the introduction of mandatory ESG information disclosure policies will become an inevitable trend.

At present, China's medium and large banks generally have had a better ESG performance, with some large state-owned banks taking a lead in areas such as granting loans to micro and small business, promoting public welfare and taking social responsibility. Medium and large banks have also performed better in terms of corporate governance, and have tighter risk-management mechanisms in place.

There has also been a trend in recent years for banks to increase investment in environmentally friendly projects with funds raised through ‘green bonds’. Fitch Bohua believes that with the Chinese government pledging to reduce carbon emission, green bond issuance in 2021 is likely to increase, and a visible ESG performance will also help banks capture the growth in the fast-growing green business.

Appendix:

1 The ASEAN countries include Malaysia, Indonesia, Thailand, the Philippines and Vietnam

2 Average GDP growth rate of the five ASEAN countries

Analyst

Meng Liu

+8610 5663 3822

meng.liu@fitchbohua.com

Yunqiao Li

+8610 5663 3821

yunqiao.li@fitchbohua.com

Joyslin Gao

+8610 5663 3820

joyslin.gao@fitchbohua.com

Li Peng

+8610 5663 3823

li.peng@fitchbohua.com

Mengyuan Wang

+8610 5663 3825

mengyuan.wang@fitchbohua.com

Frank Zhang

+8610 5663 3827

frank.zhang@fitchbohua.com

Norman Sheng

+8610 5663 3826

norman.sheng@fitchbohua.com

Disclaimer

This report is based on publicly available information or research that Fitch (China) Bohua Credit Ratings Limited ("Fitch Bohua") believes reliable. However, Fitch Bohua does not represent or warrant the accuracy or completeness of such information or materials. The opinions, assessments or forecasts contained in this report reflect the judgement and views of Fitch Bohua as at the date of this report, and at different time Fitch Bohua may issue reports that contain views or forecasts that differ with those in this report.

The information, opinions, estimates or forecasts contained in this report are for information purposes only and this report does not constitute a recommendation to any person or institution to buy, hold or sell any asset; this report does not comment on the reasonableness of market prices, the suitability of any investment, loan or security (including but not limited to any accounting and/or regulatory compliance or suitability) or the tax-exempt nature or taxability of amounts relating to any investment, loan or security. This report should not be relied upon by individuals or institutions as a factor in making investment decisions. Neither Fitch Bohua nor the relevant analysts accept any liability whatsoever for any loss or damage arising from the reliance on or use of this report.

The copyright of this report is owned by Fitch Bohua. Without Fitch Bohua’s written permission, no institution or individual may reproduce, copy, publish or quote this report in whole or in part. If Fitch Bohua's permission to quote or publish this report is obtained, it must be used within the scope of permission, with attribution to "Fitch (China) Bohua Credit Ratings Limited", and this report must not be quoted, abridged or modified in any way that is contrary to its original content. Fitch Bohua reserves all its right to claim.

The terms of this disclaimer are subject to revision and final interpretation by Fitch Bohua.